http://www.beyonddevic.es/2014/05/15/thoughts-on-sonys-q1-2014-earnings/

THOUGHTS ON SONY’S Q1 2014 EARNINGS

MAY 15, 2014 JAN DAWSON 1 COMMENT

This will probably be the last in my

series of posts about big tech companies’ Q1 2014 earnings. There was lots of press coverage of Sony’s earnings over the last several weeks, most of it for the wrong reasons – guidance revised downward, forecasting a loss for the next financial year and so on. There are plenty of pundits saying that if Sony was an American company, there would have been calls for Kaz Hirai’s resignation by now. But I wanted to take a minute and review some of the latest numbers, and highlight some of the positive trends in Sony’s business.

Sony has a reputation as a dysfunctional company (and I’ve

said as much myself), with a combination of assets that seem like they could be really powerful but with cultural, structural and political divisions between business units that have so far prevented that enormous potential from turning into real achievement. Its glory days are long since behind it, and it’s struggled both to generate a profit and to demonstrate that it can again become the powerhouse it once was.

One quick note: Sony’s financials as reported have benefited from the weakness of the Yen relative to other currencies, and so some of the revenue growth it’s seen is unrelated to the performance of its own business, so I’ll try to use other metrics in addition to revenue growth wherever possible below.

A business in many parts

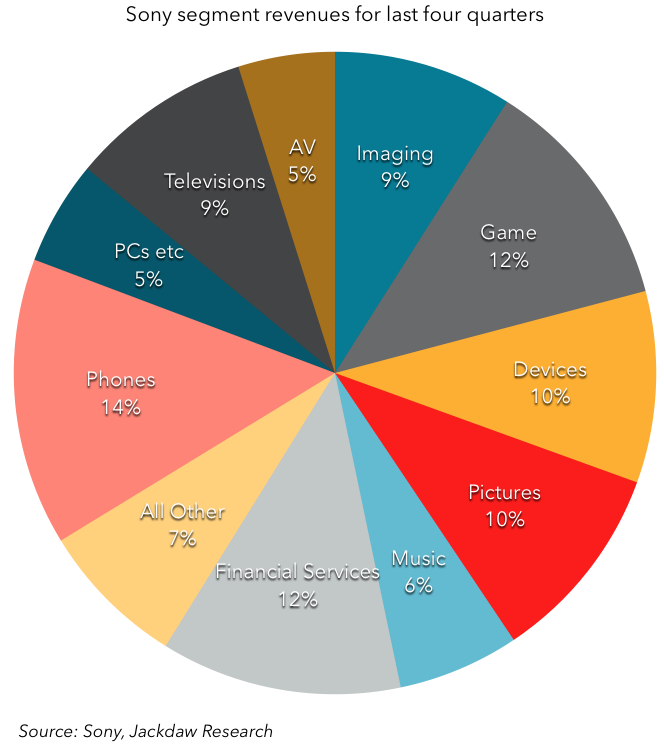

The most striking thing about Sony’s business is that it has so many parts to it – this is a company with its fingers in a lot of pies. Just look at the split of revenues shown in the pie chart below (I’ve taken some of the top-level segments and further divided them into their constituent parts because some of the sub-segments are actually quite different as well):

Look at all those businesses, with none of them generating more than 15% of overall revenues, and as diverse as financial services, electronic components, motion pictures and television sets. This enormous diversity could be both a weakness and a strength. So far it’s been a weakness, with divisions fighting rather than collaborating with each other, and creating a business that has somehow managed to be less rather than more than the sum of its parts. But latterly there have been signs that Sony is starting to get its act together and making its divisions help each other in a way they haven’t in the past. Camera and display technology from other business units have made their way into smartphones and tablets, entertainment services are now available across TVs, consoles and personal devices, and so on. There is finally evidence that Sony is starting to make its diversity pay off, though it’s still very early days.

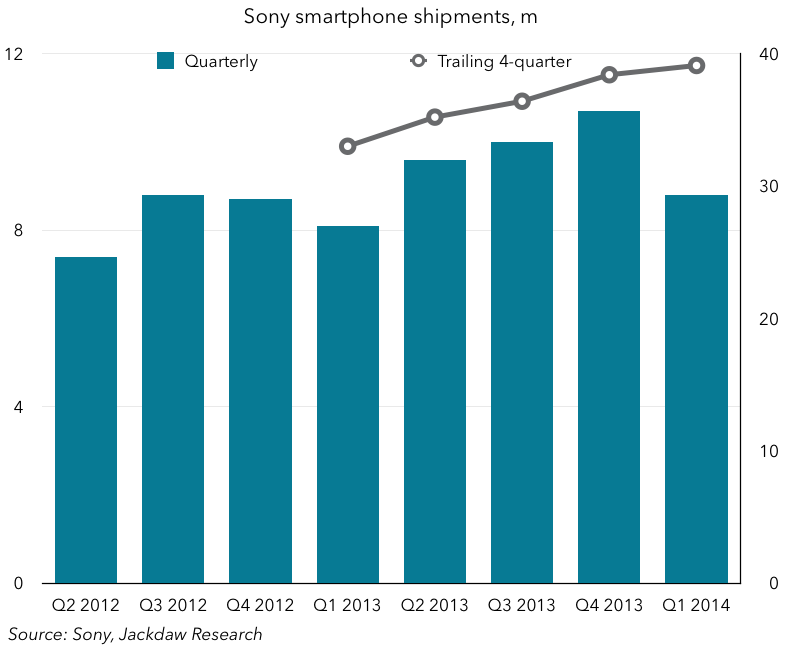

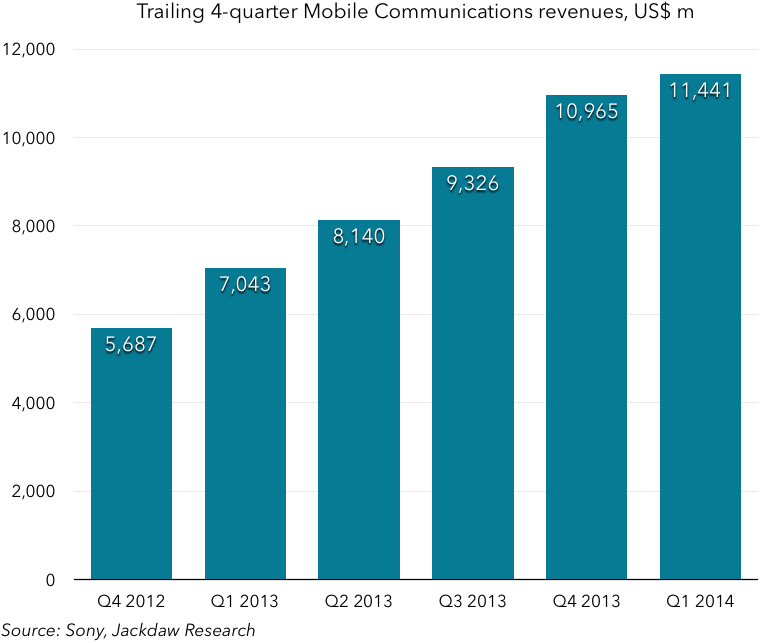

Smartphones are picking up quietly

Look at the biggest segment in the diagram above: it wouldn’t have been this way a year or two ago, but it’s now smartphones. The Sony Ericsson joint venture was a flop for the last few years of its existence, fading further and further into irrelevance, and there was a strong chance that it would suffer along with the rest of Sony’s business units when it got bought out. But that hasn’t happened. Though there’s very little fuss about it in the media, Sony has quietly been building up its smartphone business over the last couple of years – see the two diagrams below, one showing shipments and the other revenues:

When you look at trailing 4-quarter numbers like these, it eliminates the cyclical fluctuations that happen at any company in this business, and the long-term steady growth trend emerges. What’s more, the Mobile Communications business actually generated a small profit this quarter and this year. The performance of this unit has been rather buried in the overall financial reporting since it’s been lumped in with the failing PC business, but as it winds down that operation Sony is promoting the performance of its increasingly impressive smartphone business. Its performance has been further helped by the fact that average selling prices have risen from around $200 to around $300 over the past two years. Though Sony’s market share in smartphones is small – well under 10% – this is a market that’s characterized by two very large dominant players and a long tail of much smaller ones. Sony remains in the top 10 vendors globally and has shown growth over the past two years even as Samsung and others have faltered. Sony’s got its act together in smartphones and it’s really starting to pay off. It’s too early to call it a long-term success, but it’s starting to look like it might be the exception to

Horace Dediu’s rule about unprofitable smartphone vendors.

Financial services – Sony’s best business

Here’s the funniest thing about Sony: its best business has essentially nothing to do with any of the things it’s best known for – not consoles, not smartphones, not TVs, not home audio, but financial services. Have a look at these numbers (again, on a 4-quarter trailing basis):

Revenue has been climbing fairly steadily (though it took a bit of a dive this quarter), and margins have been the strongest of any of Sony’s business units, at between 15 and 20%. No other business unit comes close on a regular basis. That’s sort of a sad commentary on Sony’s other businesses in one way, but it does mean Sony has a relatively stable business, and one that’s a decent size, that can provide a good foundation even as it restructures the rest of its operations for long-term growth and profitability.

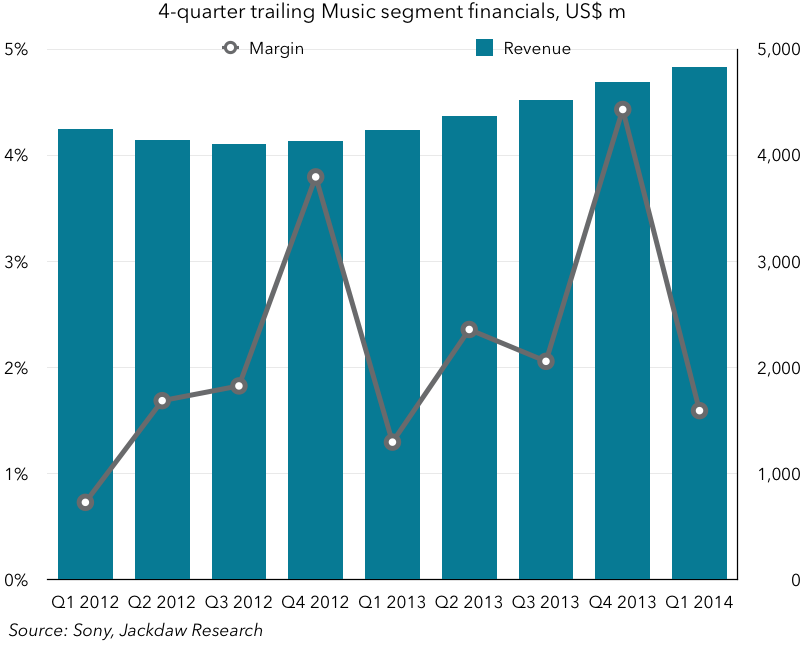

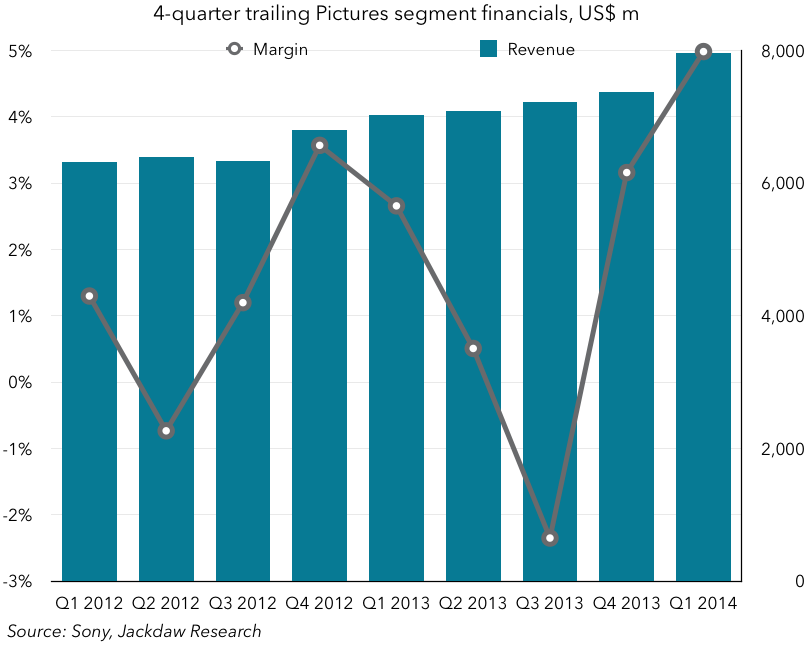

Entertainment businesses remain strong despite headwinds

Sony’s two entertainment businesses remain the next-best-performing business units after financial services. Their margins are more volatile, partly because of the hit-driven nature of both the music and movie businesses, and revenues have been fairly healthy too, even given the industry headwinds both businesses face:

Sony’s movie studio and its music business remain among the top 5 in the world in their respective fields, and this is a major strategic asset for Sony, allowing it to negotiate deals more easily by way of quid pro quo arrangements and giving it leverage other players in the consumer technology space don’t have.

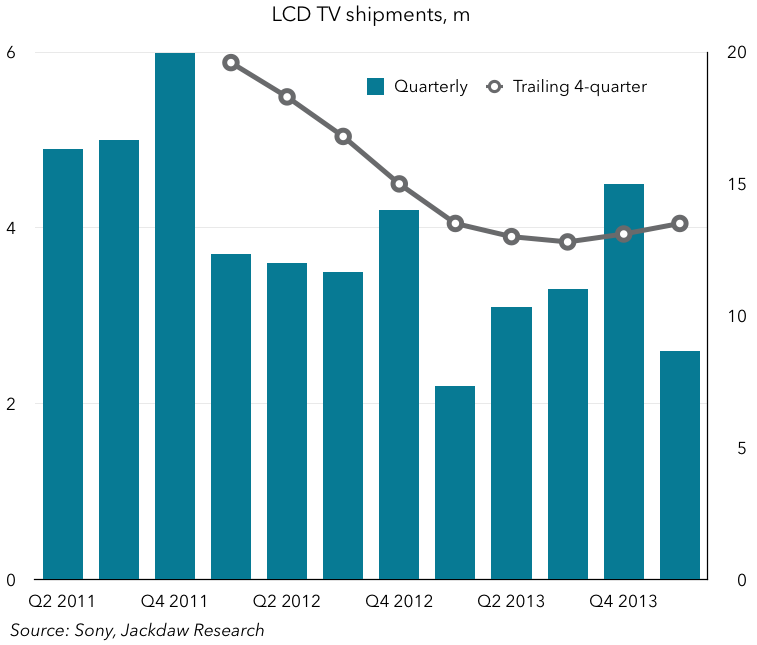

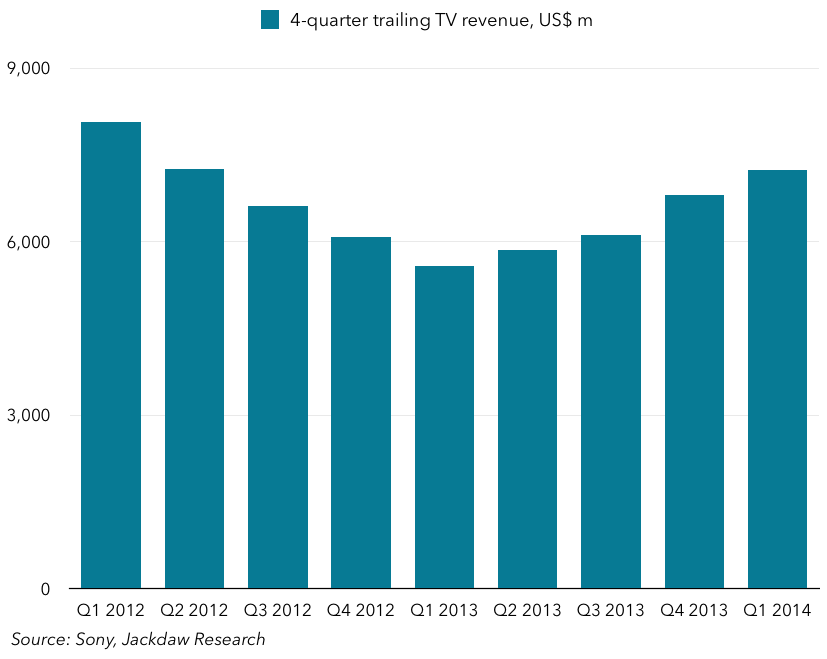

TVs are doing surprisingly well

Even as Sony decided to wind down its PC business, it decided to refocus rather than kill off its other poorly-performing hardware asset, the television set operation. The strategy here is to focus on the higher end of the market, with full HD and 4K sets, trying to leave behind some of the commoditization that has characterized the lower end of the market. Commodity Chinese vendors are already attacking the 4K space, so who knows how long this will last, but so far it might actually be working too:

As you can see, the last two quarters’ shipments were higher than the year-ago equivalents, and the trailing 4-quarter shipment line is now trending upwards as a result. That’s translated into revenue growth too (though somewhat helped by currency movements):

That’s pretty impressive for a mature business with tons of competition and thin margins. Sony hasn’t split out television set margins from its overall Home Entertainment & Sound segment, so we can’t know exactly how margins are doing, but the high end focus should help there too.

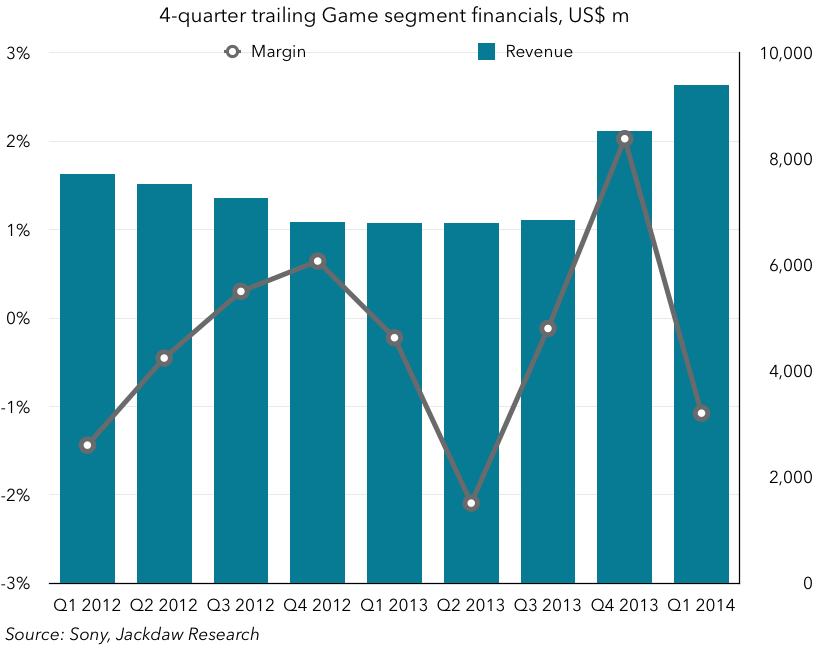

Game consoles are not doing as well as you might think

Sony’s game console sales have been generating some of the few positive headlines for the company over the last few months. Playstation has been outselling Xbox in their most recent iterations, and actually over the past two years every quarter:

Even that chart shows that the last two quarters’ shipments at Sony were only barely higher than the previous year’s shipments, despite the PS4 launch. Margins have actually declined, partly because of the upfront investment necessary to get the Playstation 4 off the ground, although revenues have started to climb in the last couple of quarters:

This is one of Sony’s highest-profile businesses, but it’s just not doing as well as you might think. For most of the last two years it’s been unprofitable, even well before the PS4 launch. And even when it is profitable, it’s only barely so. Sony needs to find more ways to boost the performance of this unit, including applying some of the same cross-segment synergy it’s used so effectively in smartphones lately. It might also usefully create a sort of Playstation Mini as a TV companion box a la Roku and Apple TV.

The outlook depends on execution

Sony’s strategy at this point is sound. All its business units except the one it’s winding down seem to be on an upward trajectory, and PCs should be fully closed within the next couple of quarters due to the accelerated pace of that action. The company is forecasting positive margins in every business unit next financial year, excluding restructuring costs, and based on the above analysis it’s possible, at least in theory. But so much will depend on the company’s execution on this strategy, and the ability to overcome strong negative trends in several of the markets Sony operates in, notably TVs, content and game consoles. Its track record of hitting its original guidance has been pretty poor over the last couple of years, but there are reasons to believe it might finally be turning a corner at last.